Regulatory Acts

These acts are designed to set standards, protect consumers, and maintain a fair and competitive market. Comprehending the scope and implications of regulatory acts is vital for ensuring legal compliance and long-term success.

Highlights

As demonstrated by the recent Credit Suisse episode, outside resolution, some Additional Tier 1 (AT1) bonds may be written down entirely before the wipe-out of Common Equity Tier 1 (CET1). This situation implies a transfer of value from holders of such AT1 bonds to shareholders.

While the isolated write-down is feasible in many jurisdictions, unintended consequences associated with the use of this mechanism may lead authorities to only write down these bonds in resolution. This would effectively deprive them of their ability to absorb losses on a going-concern basis.

Since the AT1 instruments were conceived for the purpose of absorbing losses on a going-concern basis, there may be merit in considering whether the current design of AT1 instruments remains fit for purpose or whether adjustments to the regulatory framework might be necessary.

In addition, given the potential for market misperceptions regarding the functioning of AT1 bonds, authorities may wish to consider whether there is merit in pursuing regulatory work aimed at increasing the transparency and disclosure of AT1 instruments' characteristics.

1. Introduction

On 19 March 2023, Swiss authorities announced that UBS and Credit Suisse (CS) would merge in what was described by the Swiss minister of finance as a “commercial transaction”, as opposed to a formal resolution proceeding.2 The transaction included, among other elements: (i) a full writedown of all CS-issued instruments outstanding at the time and counting towards CS Additional Tier 1 capital (AT1), affecting instruments with a total nominal amount of CHF 16 billion; and (ii) a share swap whereby CS shareholders would receive one UBS share for 22.48 CS shares, effectively recognising residual equity of CHF 3 billion for CS shareholders. 3 The writedown of CS AT1 instruments had a significant impact on the AT1 market. Yields on AT1 instruments increased substantially in the aftermath of the transaction, 4 and scheduled issuances were postponed.5 Against that background, some authorities issued statements reiterating that, in their jurisdictions, AT1 instruments rank ahead of Common Equity Tier 1 (CET1) in the hierarchy of claims in liquidation and, as a result, AT1 bondholders should expect to be exposed to losses in resolution or insolvency in the order of their positions in this hierarchy. 6 The Swiss authorities’ decision also gave rise to legal disputes initiated by AT1 bondholders and CS staff whose bonuses were tied to such instruments.7 While AT1 markets have since somewhat calmed, the episode triggered an ongoing debate on the exact conditions under which AT1 instruments contribute to restoring a bank’s viability and the mechanisms through which this is achieved. Importantly, this episode also raised the question of whether AT1 instruments can be written down “in isolation” – ie without a writedown of CET1 capital. Key in that respect is the question of whether the isolated writedown was an idiosyncratic feature of CS AT1 instruments and the specific circumstances of that bank’s failure, or whether other AT1 instruments, either on the basis of their terms or as result of how they interact with their regulatory framework, might behave in similar ways. This FSI Brief aims to contribute to this debate. It analyses a sample of AT1 instruments issued under various legal frameworks with a view to identifying the potential of isolated writedowns. Section 2 reviews, from a conceptual perspective, the conditions allowing for an isolated writedown of AT1 instruments. Section 3 takes a more practical approach and looks at regulatory frameworks in selected jurisdictions as well as the contractual terms of the aforementioned sample of instruments. Section 4 concludes.

2. Possibilities to write down AT1 instruments

The Basel Framework requires a contractual principal loss absorption mechanism for all AT1 instruments (“contractual approach”), unless the governing jurisdiction of the bank has in place laws that allow authorities to enact the conversion or writedown of these instruments irrespective of their terms and conditions (“statutory approach”). Both writedown and conversion may strengthen overall resilience and may ultimately help increase confidence in a bank’s capital strength. At the same time, if AT1 principal is written down, and unless CET1 is also written down, value is effectively transferred from AT1 bondholders to shareholders. The transfer of value results from the fact that both AT1 bondholders and shareholders have a stake in the bank’s business. As such, if the stake of AT1 bondholders is cancelled as a result of a writedown of AT1 principal and CET1 is not wiped out, then any value attached to AT1 automatically accrues to the stake of the shareholders. The transfer of value may also occur in the case of a conversion, and its magnitude will depend on the rate at which AT1 bonds are converted into shares (ie the conversion price). 8 The way value is transferred depends on the type of contractual clause that triggers the writedown. Typically, AT1 bonds have two types of trigger clauses in their terms, quantitative and qualitative: • Quantitative trigger: a contractual clause in the bond terms that provides for an automatic writedown if the issuing bank’s CET1 position falls below a specified level. The Basel Framework mandates that AT1 instruments classified as liabilities for accounting purposes (rather than equity) must contain a quantitative trigger calibrated to 5.125% CET1 or higher. If the trigger is met, the principal amount of the bond is automatically written down at least in an amount needed to restore CET1 to 5.125% or the higher contractually specified target level.9 As a result, the value attached to the amount of AT1 that is written down automatically accrues to the holders of CET1. • Qualitative trigger: a contractual clause that provides for a trigger other than a specified CET1 ratio. The rationale for this type of trigger is that, while a bank’s reported capital position may be above the regulatory minimum, a further strengthening of the capital base may be needed to restore confidence if a bank has reached the point of non-viability (PONV) in advance of falling short of regulatory capital minima or based on other criteria. The Basel Framework mandates that AT1 instruments must have contractual clauses reflecting such a qualitative trigger unless the jurisdiction of the issuing bank provides for a statutory mechanism to the same effect. It defines the PONV as the earlier of: (i) the decision of the relevant authority that a writedown is needed to restore the viability of the issuing firm: or (ii) a decision by the public sector to provide support to restore the viability of the issuing firm.10 The activation of the qualitative trigger is at the discretion of the relevant authority, and hence the possibility of a value transfer depends on whether the relevant authority is constrained in its discretion to write down the instrument without a preceding or concurrent full writedown of CET1. In that regard, two scenarios need to be distinguished: - In resolution: If the PONV as defined under the contractual terms of an AT1 instrument coincides with the conditions for resolution as defined in the relevant jurisdiction, the competent authority may decide to put the bank in resolution while simultaneously writing down the AT1 principal. In such a scenario, a transfer of value is unlikely to occur because resolution frameworks mandate that the creditor hierarchy must be respected in resolution. 11 - Outside resolution: The qualitative trigger as defined under the contractual terms of an AT1 instrument may not be fully aligned with the conditions for resolution as defined under a jurisdiction’s resolution framework. Indeed, resolution frameworks in many jurisdictions include conditions that go beyond “non-viability” and include elements such as a public interest assessment and absence of a private sector solution.12 In such a situation, a writedown of AT1 instruments without the wipe-out of CET1 may occur unless the relevant legal framework restricts such an action. Graph 1 presents a decision tree that illustrates the above logic.

3. Stocktake of AT1 loss absorption in selected jurisdictions

This section explores the potential for an isolated writedown in a sample of AT1 instruments issued primarily by global systemically important banks but also by other internationally active banks in Canada (CA), China (CN), the European Union (EU), Japan (JP), Switzerland (CH) and the United Kingdom (GB). The sample includes 173 issuances totalling aroun

3.1 Statutory and contractual approaches across selected jurisdictions

Jurisdictions have taken different approaches to implementing the loss absorption requirement. The United States applies the statutory approach to the PONV requirements. Accordingly, instruments qualifying as AT1 (eg preferred stocks) typically do not contain contractual terms establishing writedown or conversion in case of CET1 depletion or when the issuer bank reaches the PONV. Instead, loss absorption is ensured by the ability of the Federal Deposit Insurance Corporation to place failing financial institutions into receivership, and require capital instruments issued by failing banks to be written down before taxpayers are exposed to loss.13 In contrast, Canada, China, the EU, Japan, Switzerland and the United Kingdom follow a contractual approach. Consequently, in those jurisdictions the AT1’s loss absorption mechanism is specified in the terms and conditions of such instruments.

3.2 Quantitative triggers

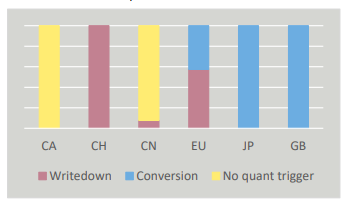

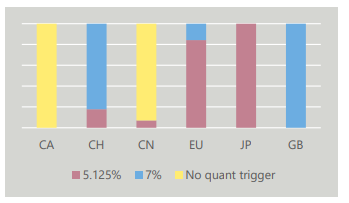

In the EU, Japan, Switzerland and the United Kingdom, regulatory frameworks determine that the contractual terms of AT1 instruments must include the provision that such instruments will be written down or converted if the issuer bank’s CET1 ratio falls below 5.125% (or a higher level specified under the contractual terms). In practice, all surveyed contracts from those jurisdictions foresee a single option for AT1 instruments to absorb losses – ie either writedown or conversion, but never both – when the quantitative threshold is breached. As a result, there is no room for discretion when the quantitative trigger event occurs (Graph 3.A). As for the actual trigger levels, while no selected jurisdiction mandates a threshold above 5.125% CET1, a significant portion of bonds in the sample triggers at 7% CET1 (Graph 3.B). These are often referred to as high-triggering bonds, as opposed to instruments with a 5.125% CET1 trigger, which are denominated low-triggering bonds.14 The Basel III standard requires quantitative triggers only for AT1 instruments that are classified as liabilities. In Canada, the regulatory framework does not require the contractual terms of AT1 instruments to contain a quantitative trigger, because the Office of the Superintendent of Financial Institutions (OSFI) considers those AT1 instruments to be equity instruments.15 This is also the situation in China, where AT1 instruments have been classified as equity since 2019. While some bonds issued before 2019 contain quantitative triggers, issuances since 2019 no longer include that type of trigger and account for the vast majority of Chinese bonds in our sample.16

3.3 Qualitative triggers

Selected jurisdictions differ as regards making qualitative triggers a mandatory element in the contractual terms of AT1 issuances. In Canada and Switzerland, regulatory frameworks require AT1 instruments to have a contractual PONV trigger and further stipulate that such qualitative triggers must be deemed met if the issuing bank, upon becoming non-viable, receives public support. 17 In China, regulatory frameworks require AT1 instruments to have a contractual PONV trigger but do not specify that it is deemed met if public support is provided. In the EU, Japan and the United Kingdom, AT1 instruments may – but are not required to – have such triggers.18 In our sample, with the exception of Chinese bonds, all issuances include qualitative triggers that contemplate scenarios where public support is provided.19 However, these clauses differ in how they define the provision of public support. The vast majority of surveyed bonds refer to the provision of extraordinary public financial support in generic terms; this could potentially include public capital support as well as public liquidity support. A smaller share of our sample specifically refers to public capital support (Graph 4.A). This may imply that the provision of extraordinary liquidity support by public authorities alone would not be a sufficient condition to activate these triggers for such instruments.

3.4 Writedown and/or conversion upon trigger activation

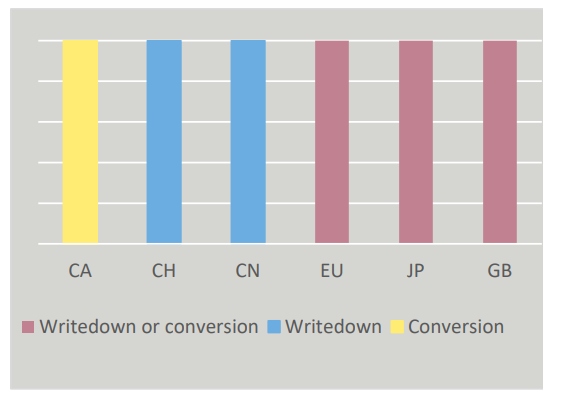

The instruments in our sample differ as to the consequences that they attach to a qualitative trigger being met. In accordance with the applicable regulatory framework, AT1 bonds issued by Canadian banks only provide for conversion into CET1, rather than writedown, if a qualitative trigger is met. 20 In other selected jurisdictions, regulatory frameworks allow the possibility for contractual terms to provide for writedown only, conversion only or both options. In practice, all surveyed contracts of AT1 instruments issued in those jurisdictions foresee the possibility of a writedown, with most of those also having the possibility of a conversion (Graph 4.B).21

3.5 Writedown outside resolution

In selected jurisdictions, the conditions for triggering the loss absorption mechanisms of AT1 instruments do not always coincide with the prerequisites for putting a bank in resolution. In some cases, the former is a necessary but not a sufficient condition. The Bank Recovery and Resolution Directive (BRRD), for example, which is the relevant framework for both the United Kingdom and EU member states, provides that the resolution authority may write down AT1 bonds “independently of resolution action”.22 In addition, and notwithstanding the fact that all triggers refer to the issuer becoming non-viable, no surveyed contract establishes resolution action as a pre-condition for AT1 instruments to be written down or makes a writedown of AT1 contingent on the writedown of CET1. In fact, in many cases in our sample, prospectuses explicitly indicate that a writedown may occur without the relevant authorities taking any resolution action. Consequently, if a qualitative trigger is deemed met but the relevant authorities consider the conditions for resolution not to be met or choose not to take any resolution action, an isolated writedown of AT1 instruments is a possibility, provided that there are no restrictions on such actions in the relevant legal framework

3.6 Legal restrictions

Legal provisions may restrict authorities’ ability to write down AT1 instruments without the wipe-out of CET1. The BRRD, for example, while allowing for a writedown “independently of resolution action” (see above), mandates that, irrespective of whether a writedown occurs within or outside resolution, CET1 must be written down first.23 Yet there appears to be no mechanism in place that enables authorities – in the EU or elsewhere – to achieve such a writedown of CET1 outside resolution. This seems to imply that, if authorities wish to avoid an isolated writedown of AT1 (and the transfer of value associated with it), they would have to take a resolution action whenever they chose to write down AT1.

4. Conclusions

In principle, an isolated writedown of AT1 instruments, and hence a transfer of value, is possible under specific circumstances in most jurisdictions analysed in this paper. This would be the case in the EU, Japan, Switzerland and the United Kingdom upon the occurrence of a quantitative trigger event, if such event was to take place outside resolution. Experience shows, however, that this would be an improbable event as authorities are likely to take a resolution action before capital adequacy ratios breach trigger levels. Nevertheless, an isolated writedown would be feasible in China, Japan and Switzerland (but not in the EU or the United Kingdom), if authorities in those jurisdictions were to write down AT1 instruments on the basis of the qualitative trigger before putting the failing bank in resolution. In practice, however, some authorities may wish to avoid the transfer of value from AT1 bondholders to shareholders. This stance may be justified, for example, on the basis of concerns about negative market reactions and the functioning of AT1 markets. This, in turn, would imply that authorities would only impose losses on AT1 instruments as part of a resolution action. This is because authorities lack powers to impose losses on shareholders outside resolution. This seems to imply that most AT1 bonds would in practice become an instrument with limited capacity to absorb losses on a going-concern basis. Since the AT1 standard was designed precisely for the purpose of absorbing losses on a going-concern basis, there may be merit in considering whether the current design of AT1 instruments remains fit for purpose or whether adjustments to the regulatory framework might be necessary. Moreover, the market reaction following the decision by Swiss authorities to write down CS AT1 instruments seems to suggest that some market participants may not fully appreciate that, while broadly similar, writedown conditions may differ across AT1 instruments. As a result, national authorities and standard-setting bodies may wish to consider whether there is merit in pursuing further work to increase the transparency and disclosure of AT1 instruments’ characteristics with a view to improving the functioning of the markets for these instruments

1. Introduction